Missed Super Contributions? How to Catch Up and Build Wealth

Financial Planning

Read time 4mins

Back to Insight

Now Reading:

Missed Super Contributions? How to Catch Up and Build Wealth

The benefits of starting early in superannuation are clear, as the power of compounding, combined with its tax-efficient structure, makes early investment compelling. However, many individuals delay contributions due to other financial priorities, such as education, cost-of-living pressures, property purchases, and raising children. The ability to use carry-forward contributions provides an opportunity to ‘catch up’ by making larger one-off deposits into superannuation, which can help grow your balance and provide tax savings.

What are carry forward contributions?

Concessional contributions typically include those made by an employer, salary sacrifice arrangements, or personal transfers where a tax deduction is claimed. The effect is to reduce your taxable income and thus, provide tax savings. Due to their attractiveness, limits are in place to govern the maximum amount that can be contributed to superannuation in this way. For the current financial year (ending 30 June 2025), this limit is $30,000.

A carry-forward contribution allows individuals to ‘catch up’ by making contributions beyond the current year’s limit, using unused portions of the cap from the previous five years. To be eligible to carry forward unused contributions, an individual must have:

- A total super balance of less than $500,000 at 30 June of the previous financial year.

- Unused concessional contributions cap amounts from up to 5 previous years.

How can carry forward contributions be used?

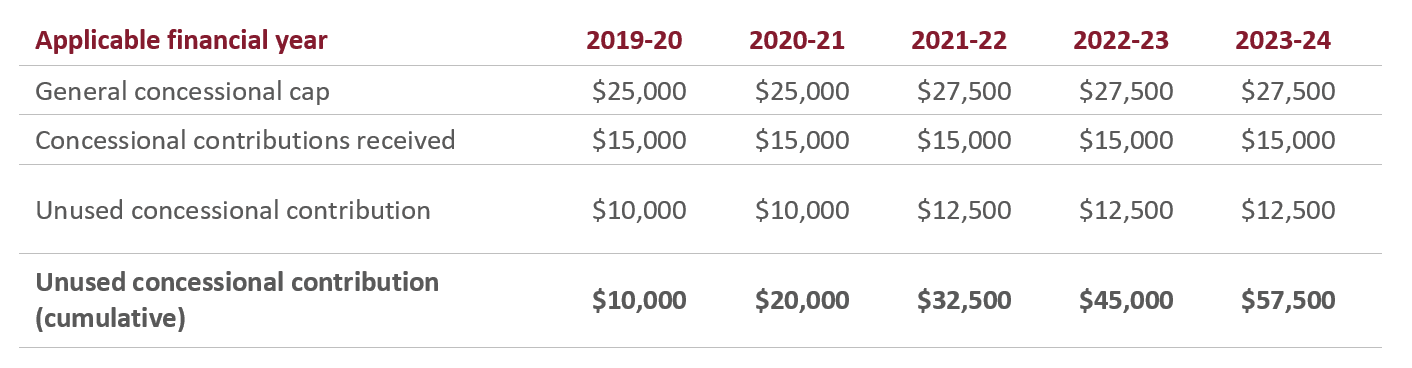

Individuals who have not maximised their contributions over the past five years can take advantage of this strategy. Importantly, the provision operates on a ‘use it or lose it’ basis, with unused contribution caps progressively forfeited. As a result, the current financial year is the final opportunity to utilise unused amounts from 2019–20.

For example, Riley has received super contributions of $15,000 from her employer in each of the past five years. After recently selling an apartment, she now wishes to contribute additional funds to her superannuation. Without using her carry-forward limits, she would be able to make a concessional contribution of $30,000. However, by leveraging this strategy, she can contribute an additional $57,500.

Source: E&P

Please note, the above table is for illustrative purposes only and does not constitute advice.

Benefits of carry forward contributions

An individual like Riley benefits in two ways from making a carry-forward contribution. In the short term, she gains personal tax savings, while in the long term, her superannuation balance grows significantly.

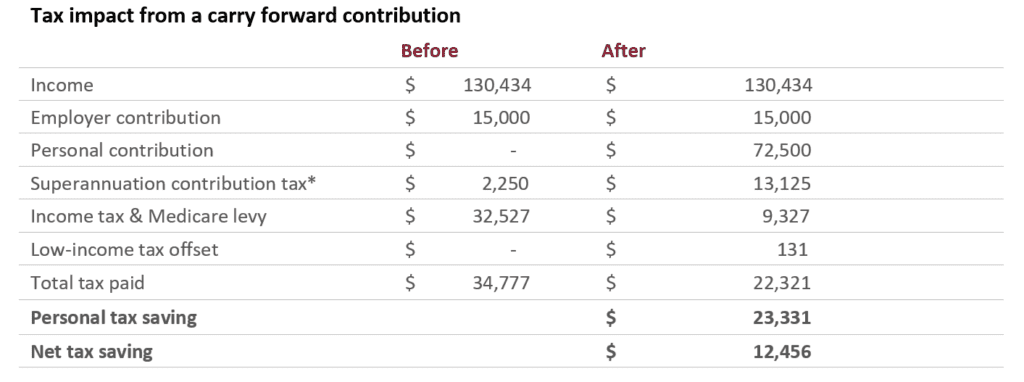

From a tax perspective, the table below outlines Riley’s financial position. She currently earns $145,434 per annum (including super) and was able to sell her apartment without incurring capital gains tax, thanks to the ‘six-year rule.’ This rule allows Riley to continue treating the rented apartment as her principal place of residence for tax purposes for up to six years after moving out. As a result, Riley contributes $72,500 to her super fund. This figure reflects her maximum allowable contribution based on the current year’s concessional cap of $30,000, her carry-forward amount of $57,500, less the $15,000 she will receive from her employer contributions.

When Riley submits her tax return for the 2024–25 financial year, she will receive an estimated tax saving of approximately $23,000.

Source: E&P

* Please note, the above table is for illustrative purposes only and does not constitute advice. Deposits made to an accumulation account attract a contribution tax of 15% that is paid from the super fund.

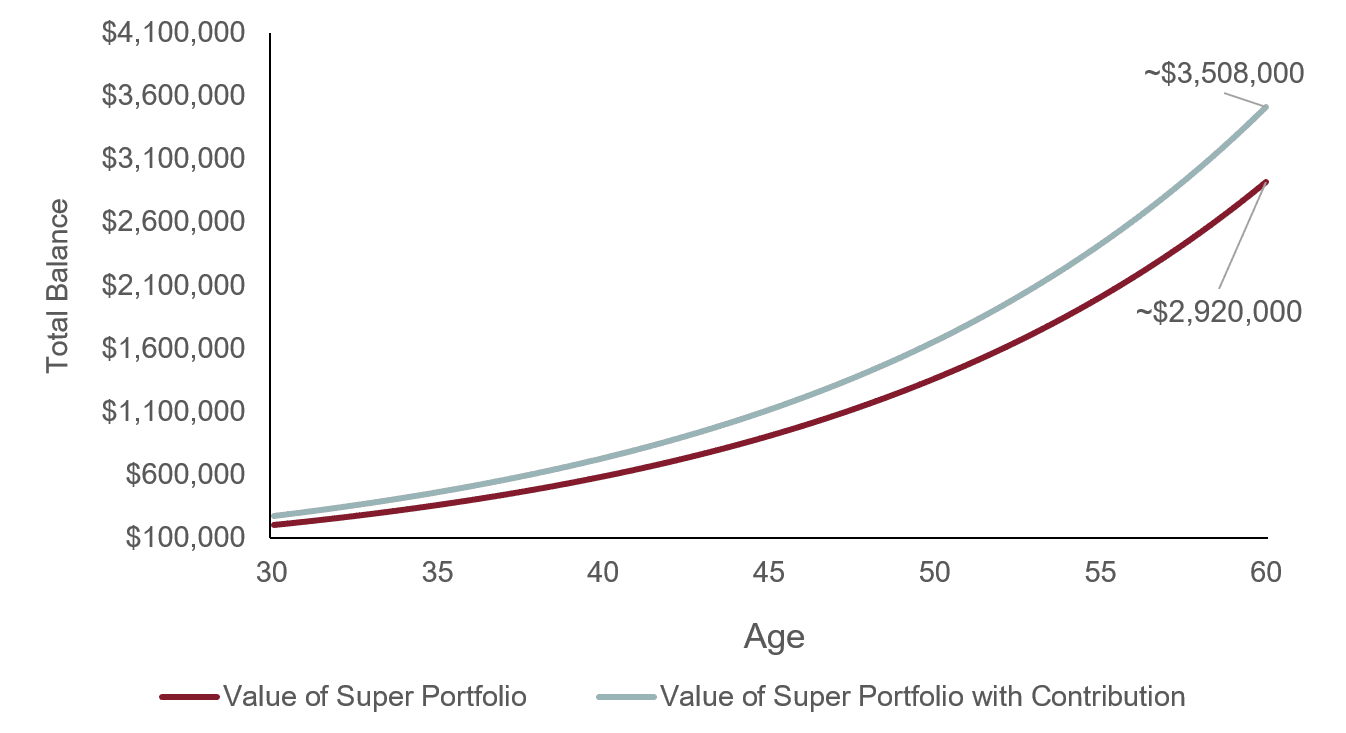

In the long term, Riley also builds significant wealth within her superannuation. With an initial balance of $200,000, regular employer contributions of $15,000 per year, and an assumed annual return of 7%, her superannuation grows to over $2.9 million in 30 years. However, by making the additional contribution now, her balance reaches $3.5 million—an extra $600,000 from her $72,500 contribution.

Source: E&P

Please note, the above graph is for illustrative purposes only and does not constitute advice. The actual outcome will vary based on market movements, fees, insurance premiums, tax paid, and your relevant personal circumstances. The 7% return used in this example is not applicable to all investment returns. Individual performance may also differ due to timing of transactions or investment size of holdings.

Riley is able to make a large superannuation contribution following the sale of her apartment. Although favourable, not all individuals have this strong asset base to leverage and have instead relied on assistance from family. According to the Finder Wealth Building Report 2024, 34% of Australian parents have bought investments on behalf of their offspring. Our Insight on Gifting explores how parents can assist.

Overview

The carry forward provision is an effective strategy for individuals looking to build their superannuation, minimise their tax liability, and secure their financial future. An Evans and Partners financial adviser can offer expert guidance on concessional caps and carry-forward rules, helping you align your cash flow management with your long-term financial goals.

Featured Insights

View all Insights

Internship Program - Expression of Interest

Fill out this expression of interest and you will be alerted when applications open later in the year.

Help me find an SMSF accountant

Begin a conversation with an accountant who can help you with your self-managed super fund.

Media Enquiry

Help me find an adviser

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to insights

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Start a conversation

Reach out and start a conversation with one of our experienced team.

Connect to adviser

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.

Contact Jacie Tran

Team Assistant, Corporate Advisory

Contact Justin To

Associate, Corporate Advisory

Contact Mark Connors

Managing Director, Senior Investment Adviser and Head of Private Wealth Management, Brisbane

Contact Hibah Jamal

Investment Adviser

Contact Jessica Scott

Associate, Consumer

Contact Luke Fussell

Associate Adviser

Contact Giorgio Antoci

Associate, Research

Contact Adam Howard

Associate, Corporate Advisory

Contact Mike Adams

General Counsel & Joint Company Secretary

Contact Robert Darwell

Chief Financial Officer & Joint Company Secretary

Contact Shankari Thayakaran

Associate, Small Caps

Contact Miquela Bezuidenhoudt

Associate, Capital Markets

Contact Annabel Khun

Associate, Technology

Contact Nick Torelli

Associate, Transport & Infrastructure

Contact Hamish Frazer

Associate, Media & Telco

Contact Genevieve Perrignon

Analyst, Corporate Advisory

Contact Richard Trinder

Analyst, Capital Markets

Contact Daniel Jetter

Director, Fixed Income

Contact Entcho Raykovski

Executive Director, Media & Telco

Contact Anthony Chiefari

Director, Senior Investment Adviser & Product Review Group Secretary

Contact James Morrow

Executive Director, Senior Investment Adviser, Investment Committee Secretary & Product Review Group Member

Contact Ben Keeble

CEO and Managing Director

Contact Caleb Adams

Director, ESG & Sustainable Investment

Contact Tiana Moini

Team Assistant

Contact Paris Gutierrez

Associate Director – Senior Specialist, Corporate Access

Contact Tanya Irvine

Executive Director, Head of Corporate Access

Contact Taylor Duong

Associate Director, Institutional Middle Office

Contact Stephanie Siomos

Associate Director, Fixed Income

Contact Stefan Cvetkovic

Associate Director, Fixed Income

Contact James O’Hare

Managing Director, Head of Fixed Income

Contact Simon Bernadou

Associate Director, Institutional DTR

Contact Mark Steer

Director, Sales Trader

Contact Alexander Blight

Executive Director, Sales Trader

Contact Steven Marchio

Executive Director – Institutional Equities Sales

Contact Anna Lenzner

Executive Director, Institutional Equities Sales

Contact Bill Forde

Executive Director, Institutional Equities Sales

Contact Will Hart

Executive Director, ESG & Sustainable Investment

Contact Sam Fletcher

Managing Director, Institutional Equities Sales

Contact Adam Woods

Managing Director, Head of Sales Trading

Contact Anne Anderson

Independent Member, Investment Committee

Contact Honor McFadyen

Independent Chair, Investment Committee

Contact Natalie Virgona

Desktop Publisher, Corporate Advisory

Contact Buddhika Ratnasekara

Analyst, Corporate Advisory

Contact Harshit Taneja

Analyst, Corporate Advisory

Contact Samuel Long

Associate, Corporate Advisory

Contact Brad Hancock

Director, Corporate Advisory

Contact Stephanie Kelaher

Director, Corporate Advisory

Contact Andrew Serle

Executive Director, Capital Markets

Contact Nicholas Zaita

Executive Director, Corporate Advisory

Contact Tom Washington

Executive Director, Corporate Advisory

Contact Angus Buckley

Managing Director, Co-Head of Corporate Advisory

Contact Peter Jorgensen

Managing Director - Head of Private Wealth Sydney, Senior Investment Adviser

Contact Andrew Moir

Managing Director, Senior Investment Adviser, Investment Committee Member, Product Review Group Chair

Contact Nick Gordon

Managing Director - Head of Private Wealth Melbourne, Senior Investment Adviser

Contact Alex Rock

Managing Director, Co-Head of E&P Capital

Contact Olivia Cartwright

Director, Australian Institutional Sales

Contact Sam Bradshaw

Associate, Media & Gaming

Contact Branko Skocic

Associate, Energy

Contact Kade Madigan

Associate, Consumer

Contact Kieran Harris

Associate Director, Small Caps

Contact Harry Saunders

Associate Director, Building Materials & Services

Contact Max Casey

Executive Director, Portfolio Strategist

Contact David Nayagam

Executive Director, Healthcare

Contact Adam Martin

Executive Director, Energy

Contact Tim Rocks

Chief Investment Officer

Contact Robin Young

Executive Director, Research

Contact Olivier Coulon

Executive Director, Small Caps

Contact Phillip Kimber

Executive Director, Consumer

Contact Paul Mason

Managing Director, Technology

Contact Julian Mulcahy

Managing Director, Small Caps

Contact Cameron McDonald

Managing Director, Head of Research

Contact Alex Maclachlan

Managing Director & CEO – E&P Funds

Contact Paul Ryan

Managing Director & CEO – E&P Wealth

Contact Ben Keeble

CEO and Managing Director

Contact Francis Araullo

Chief Risk Officer

Contact Rose Clark

Chief People Officer

Contact Sally McCutchan

Independent Non-Executive Director

Contact Josephine Linden

Independent Non-Executive Director

Contact Tony Johnson

Non-Executive Director

Contact David Evans

Non-Executive Chairman